Clearly, we are seeing some volatility and drawdowns today and we may have to make some moves today. The obvious question is what happens next. The first thing I remind myself to do though is IGNORE THE NOISE! Good investors don’t make decisions based on what their portfolio did today.

As of writing this at 10:38 AM Eastern my personal accounts are down by over $20,000. That is about 4 times the value of my daily driver car! It is natural to have that stress me out a bit. But let me say it again, “good investors don’t make decisions based on what their portfolio did today.”

For the most part I think technical analysis alone doesn’t provide higher rates of return. This isn’t always true, but on average I believe technical analysis provides lower rates of return when you factor in costs, taxes, and missed opportunities.

Take for example the chart below. In red we can see TQQQ. In blue we can see a simple 200 day moving average model applied to TQQQ. Which one has a higher rate of return? The obvious benefit of the technical analysis system is that it has a better max drawdown. That is a big win. Likewise, a system like that could prevent an even larger drawdown that the buy and hold would likely experience in a period like the dot com bust.

Naturally some want to then trade more frequently. So, let’s look at a strategy where we follow the 50 day sma. In this we can see the drawdown is about the same, but the CAGR is much worse.

This pattern continues if we shorten the SMA to a 10-day sma.

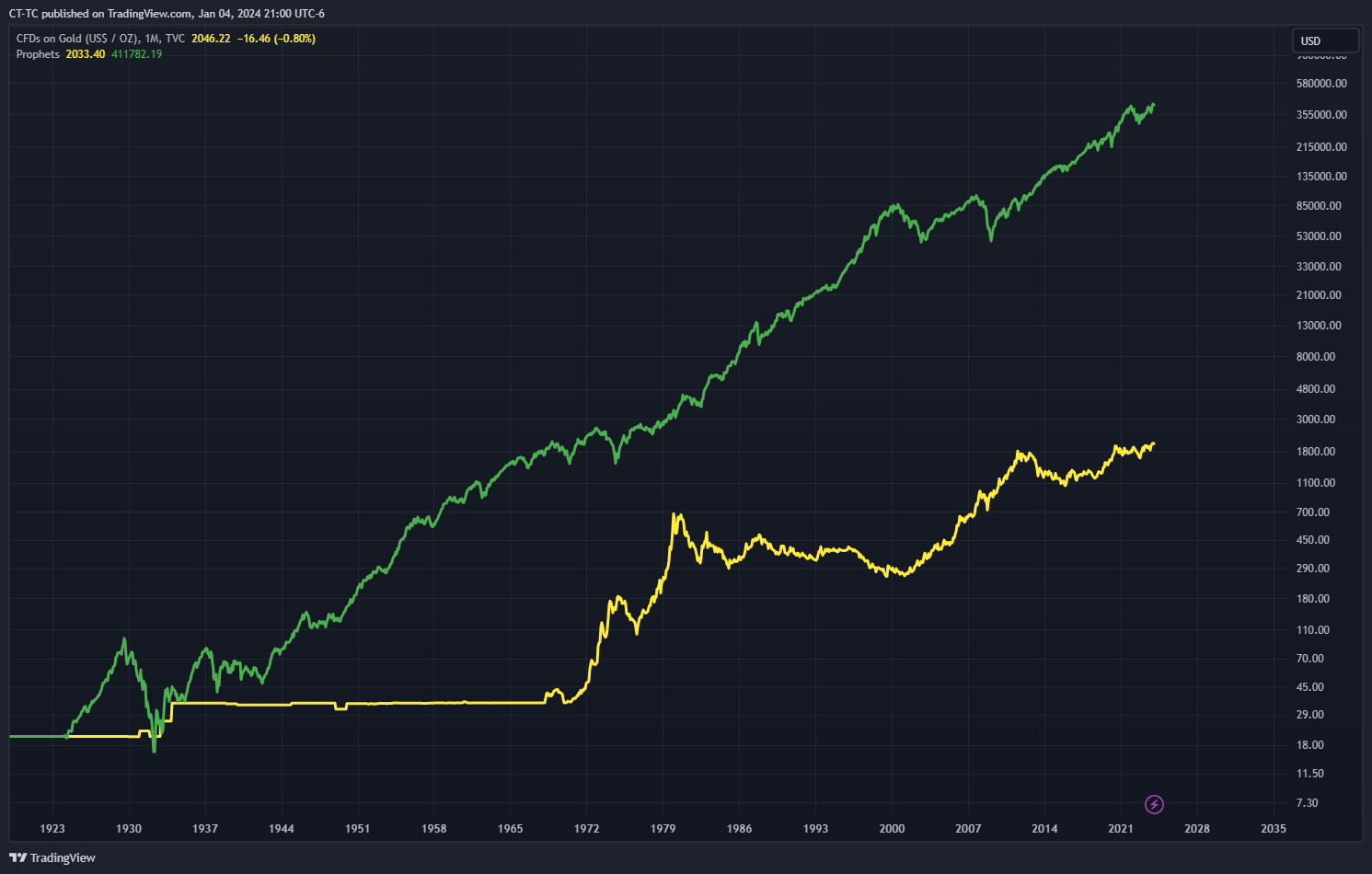

Now there are obviously ways to better utilize the 10-day sma and rotate into other assets etc. However, in general I believe there is this sweet spot. You don’t want to be a buy and hold investor with leverage, but you also don’t want to be a day trader with leverage. The downside of this sweet spot is that you will have days where you have sudden 5% drawdowns and on rare occasions larger than 10%. That just isn’t suitable for most people and that is okay. However, it is okay for me. Fortunately, I have been doing this long enough that I am able to roll with the punches. I didn’t really start trading this way until 2019, but once I did, I started to notice huge improvements. There is no covering up of the fact that 2022 was a rough year. But, in a longer-term context I think it makes sense. Take a look at this chart below of using 50/50 stocks and bonds with 3X leverage simulated going back to the 70s (source). This isn’t a perfect simulation as this free tool only allows flat leverage costs etc. However, it is a helpful demonstration. See how much money was made using leverage vs using the S&P 500. But look at the second chart below and tell me which year was the worst year for the leveraged portfolio. It was 2022. I mentioned this in 2022 and said it doesn’t mean 2023 is going to be bad. 2023 turned out to be great.

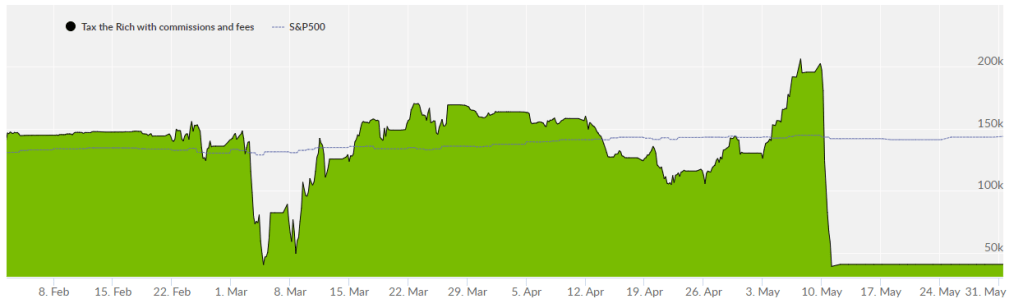

I have a host of signals I use in my algorithms. I don’t plan to share them all, but I will show my results. Below you can see a screenshot of my portfolio analyst report. In 2019, I started investing with my current approach and it has done wonders for me. I use this approach in my IRAs, HSAs, and taxable accounts. If you want to follow along you can use the blog or my links to my C2 strategies.

So I know on days like today people get jittery. I do too. We could be at the beginning of a 20% drawdown for my strategies. Or we could be about to experience a 20% launch. It is impossible to know. After the fed meeting today we may get some buy or sell signals. I do not know the future. Either way I will be sticking with my algorithms as I think they are my best chance to make money in the long run based on my extensive backtesting and live experience. I will not be taking trades because just because there has been a drawdown or because someone that hasn’t beat the S&P 500 thinks I should have tighter stops.

Disclaimer

This is not investment advice for you. This website is designed to talk about investments but it is not designed to give you personalized investment advice. This site contains generic information that does not have the capability of taking your personal risk tolerance, goals, assets, or other factors into account. Therefore, this site and all of its related content is for entertainment, informational, and educational purposes only.

The owner of PatienceToInvest.com is also a trade leader on Collective2.com. We may receive compensation by promoting some collective2 strategies over others. Should you decide to make or avoid any investments or use any service due to the information on this site or related information you assume full responsibility and risks and will not hold howiinvest.com it’s associated sites or its owners responsible. You also acknowledge investing is risky and can result in the loss of all your capital and even more than your original capital in some cases.

{kind=link}