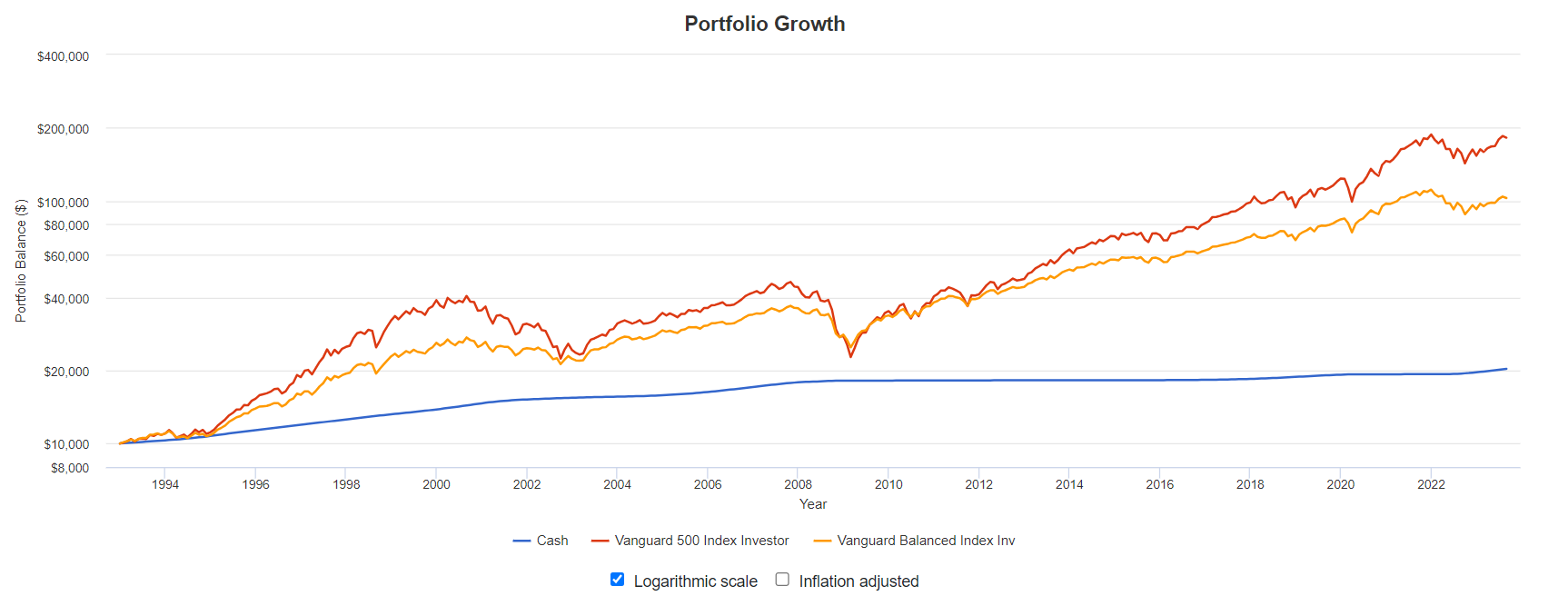

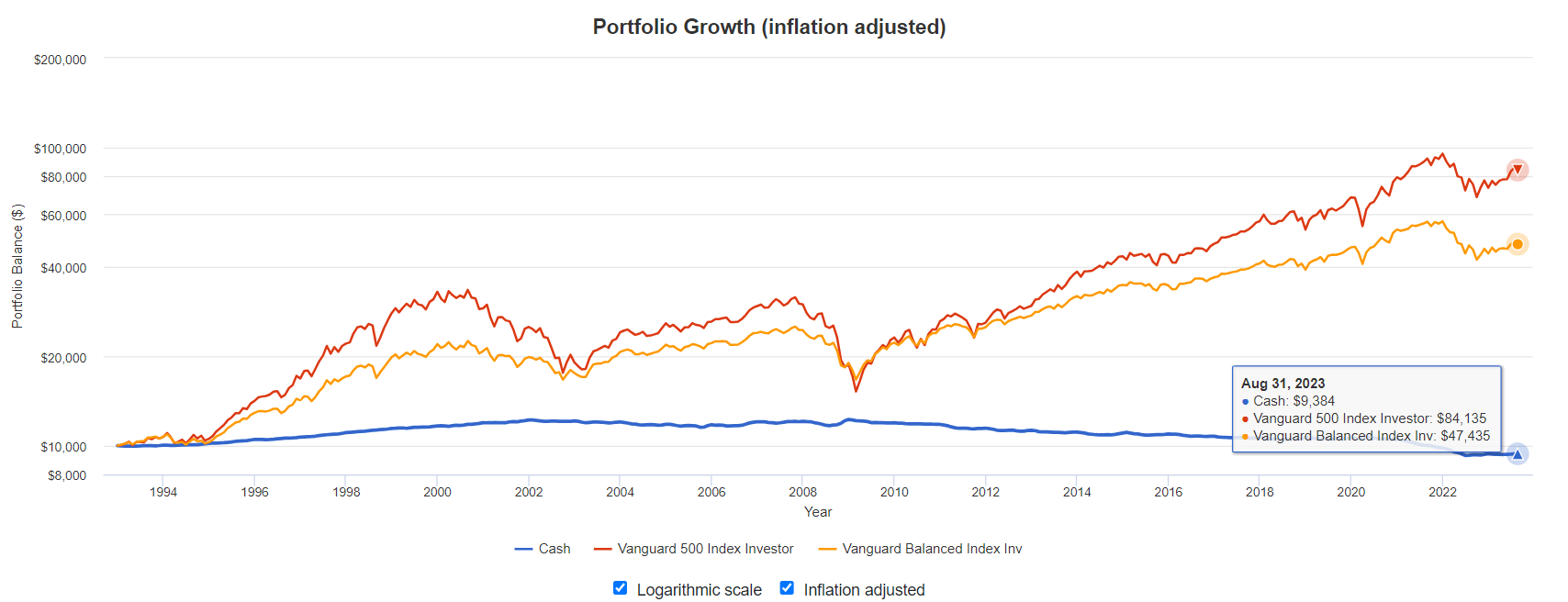

Switching from one strategy to another because one performed better in the last handful of years is killing your long-term results. It’s essential to have a solid thesis behind any strategy you choose and let that be the reason for switching – not performance. Some methodologies can perform exceptionally well over five, ten, or even twenty years with inherent risks that outweigh the benefits. Many investment strategies thrive solely because they happen to coincide with a period of good fortune – not skill and not an edge. You have to learn how to identify the difference, which is without a doubt very difficult.

This is something we often see play out on platforms like C2, where hundreds of new strategies start, most fail, and a few survive for several years. People naturally think the ones that have survived for 4 or 5 years have an edge. However, it is rare that even the successful strategies that last for five years truly have an edge.

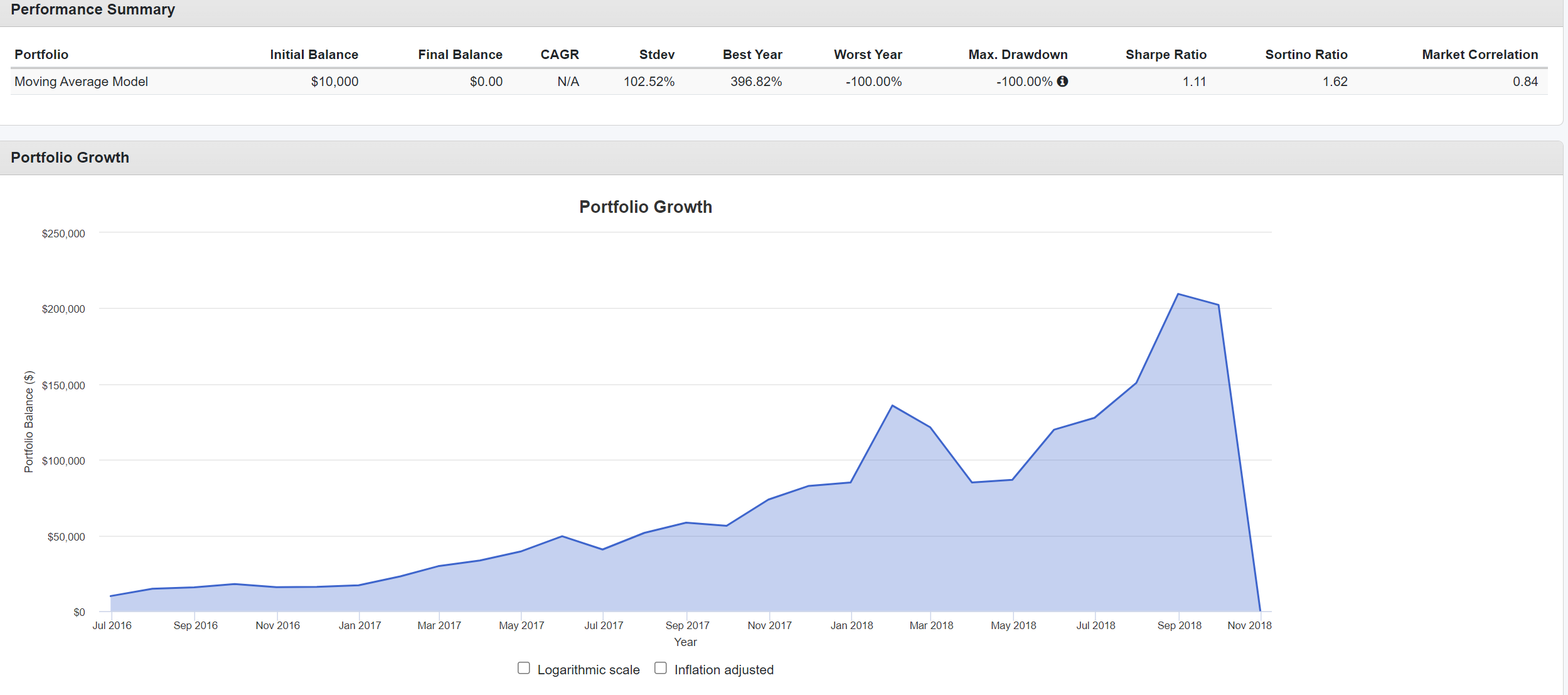

Consider a leveraged trend-following strategy trading the Nasdaq with 7x average leverage. This particular strategy would have had an annualized return of almost 116% for the last 4 years. Impressive, right? No!

This period was unusually favorable for that strategy. If we look further back, we see that it would have gone bankrupt almost three times in the last few decades.

The failure of a system mostly trading the Nasdaq with 7 times average leverage is highly likely in the long-term. It’s hard to beat an index in the long-run, and if you’re trading the Nasdaq with an average leverage of 7X, your index isn’t the S&P 500 anymore. A realistic comparison is 7X the Nasdaq with some simple trend following, which has terrible long-term results as you can see. You could try shorting the index too, but an index of shorting the Nasdaq with any level of leverage is horrendous, trend-following or not.

It’s crucial to thoroughly understand the risks associated with the trading methodologies you follow and to not follow a strategy simply because line go up, or quitting a strategy because line go down. And when I say strategy I don’t just mean a C2 strategy. This applies to mutual funds in your 401(k), C2 strategies, etc.

PortfolioVisualizer Link for the Backtest

Disclaimer

This is not investment advice for you. This website is designed to talk about investments but it is not designed to give you personalized investment advice. This site contains generic information that does not have the capability of taking your personal risk tolerance, goals, assets, or other factors into account. Therefore, this site and all of its related content is for entertainment, informational, and educational purposes only.

The owner of PatienceToInvest.com is also a trade leader on Collective2.com. We may receive compensation by promoting some collective2 strategies over others. Should you decide to make or avoid any investments or use any service due to the information on this site or related information you assume full responsibility and risks and will not hold howiinvest.com it’s associated sites or its owners responsible. You also acknowledge investing is risky and can result in the loss of all your capital and even more than your original capital in some cases.