My first low-effort attempt to track SVIX using VXX puts is due for a check-in. It would be really nice to be able to use VXX puts instead of SVIX, as it would remove the need for K-1 forms and provide better risk management. The premium cost may be too expensive to achieve a similar growth curve. Let’s take a look.

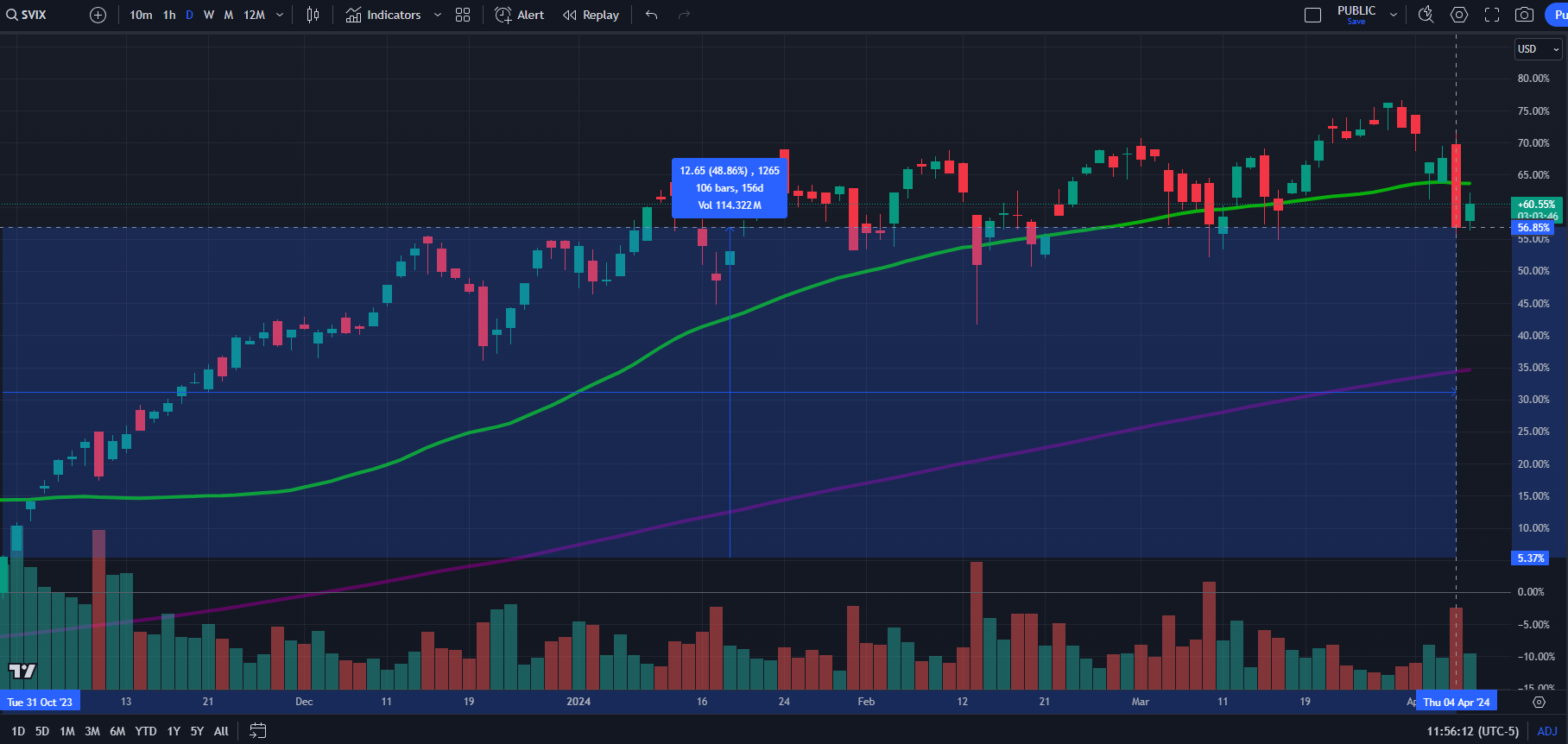

I’m going to compare the period from October 31st, 2023, to the close on April 4th, 2024. I can see that the return was about 49%. Not bad!

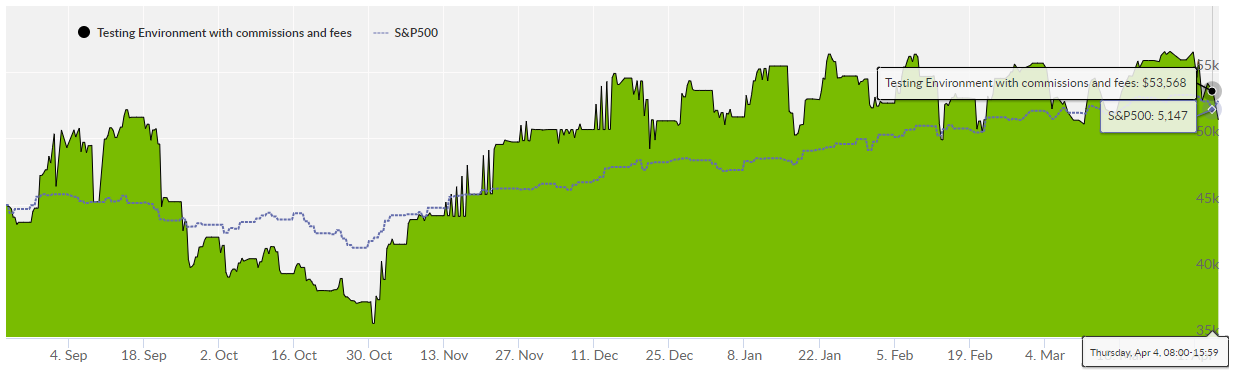

Per the two screenshots below in the Testing environment strategy , the starting equity value was $38,094. The value at the close of the period was $53,568. That is a return of 41%. That represents an 8% gap, but it could be worth it for those times when losses are sudden in SVIX. Puts on VXX could help you always have a lower maximum possible loss.

Remarks

There is the downside that when things churn sideways, such as Year-to-Date (YTD), the options setup tends to lose a bit more. For example, YTD, the test is lagging behind SVIX, which has been rather choppy and sideways year to date. The big benefit, though, is the low amount of capital needed to deploy or risk. As shown in the leverage overlay below, the amount of capital at risk is much smaller.

I don’t think using more puts over ETFs is a clear win or loss yet in this situation, but it does show some promise. It’s enough for me to keep the test going. I am also deploying a small amount of live capital so that I can get better data on actual fill prices for options instead of simulated ones. In the next update, I will compare my results at IBKR versus SVIX from today onward. This could make a significant difference with options. For example today I purchased the Jun 21, 2024 VXX puts at a strike of $20 with a cost of $6.81. When placing that same trade in C2 a few minutes apart and without any major move in VXX I the price was $7.00. As I write this the spread is about $0.40. IBKR does a decent job of not making me absorb the full spread whereas the simulation in C2 absent IBKR data does. I could also do a bit more to make sure I am holding options with ideal time to expiration to avoid excess cash at risk and time decay. Hopefully with those changes I can get the results to match more closely between synthetic SVIX and actual.

See the previous post for more information.

Disclaimer

This is not investment advice for you. This website is designed to talk about investments but it is not designed to give you personalized investment advice. This site contains generic information that does not have the capability of taking your personal risk tolerance, goals, assets, or other factors into account. Therefore, this site and all of its related content is for entertainment, informational, and educational purposes only.

The owner of PatienceToInvest.com is also a trade leader on Collective2.com. We may receive compensation by promoting some collective2 strategies over others. Should you decide to make or avoid any investments or use any service due to the information on this site or related information you assume full responsibility and risks and will not hold howiinvest.com it’s associated sites or its owners responsible. You also acknowledge investing is risky and can result in the loss of all your capital and even more than your original capital in some cases.